Updated for accuracy, market trends, and buyer safety

Last updated: 12/6/25

Insuring a classic Chevy isn’t the same as insuring a modern daily driver — not even close.

As someone who has insured multiple classics, including a 1957 Bel Air, a 1966 Chevelle, and a 1972 C10, I’ve learned (sometimes the hard way) what matters most when choosing the right insurance policy.

This guide explains:

- The different types of classic car coverage

- What insurance companies really look for

- What affects premiums

- How “agreed value” actually works

- How to insure project cars

- Common mistakes I see Chevy owners make

- Real-world examples from my own insurance experiences

By the end, you’ll know exactly what coverage you need — and how to prevent painful, expensive surprises after a loss.

Table of Contents

Why You Need Classic Chevy Insurance (Not Regular Auto Coverage)

Your ’55 Chevy Bel Air or ’69 Camaro SS doesn’t behave like a daily-driven modern car—and neither should its insurance policy.

Classic Chevys:

- Increase in value or remain stable, rather than depreciate

- Are driven occasionally, not 12–15k miles per year

- Require specialty labor and hard-to-find parts

- Often sit in a garage or storage unit most of the time

This is why top insurers offer collector car insurance specifically for classic Chevys.

Most standard auto insurance policies insure vehicles at Actual Cash Value (ACV) — which factors in depreciation.

Classic Chevys appreciate instead of depreciate. That means:

❌ A standard policy will not pay you what your classic is truly worth

✔️ A classic-car policy locks in the true value of your vehicle

This is why you must use a classic car insurer or an insurer with a specialty division — Hagerty, American Collectors, Grundy, or a classic-car program offered by your major insurer.

Agreed Value: The Foundation of Classic Chevy Insurance

The #1 feature you MUST have in classic Chevy insurance is agreed value (or guaranteed value) coverage.

Why “Agreed Value” Matters

Standard auto insurance pays actual cash value, which depreciates your car like it’s a 15-year-old minivan.

With agreed value:

- You and the insurer agree upfront on your Chevy’s true worth

- If your car is totaled or stolen, you receive the full agreed amount

- No depreciation. No arguing with adjusters.

This is critical for:

- 1955–1957 Tri-Five Chevys

- 1967–1969 Camaros

- 1964–1972 Chevelles

- Classic C10 and C/K trucks

These models see rising values, and agreed value ensures you’re fully protected.

Does Your Chevy Qualify for Collector Car Insurance?

Most insurers have similar requirements for Chevy collector car insurance:

1. Age of the Vehicle

Typically 25–30+ years old:

- ’55–’57 Bel Air

- ’60s Impala

- ’67–’69 Camaro

- ’70–’72 Chevelle

- Pre-1980 C10 trucks

Some newer limited-production Chevys (SS, ZL1, Z/28, certain Corvettes) may also qualify as “modern classics.”

2. Limited Use and Mileage

Collector policies assume hobby use:

- Weekend drives

- Car shows

- Club events

- Cruise nights

Annual mileage tiers often include 1,000 / 3,000 / 5,000 miles per year.

3. Storage Requirements

Insurers almost always require:

- Garage, barn, storage building, or secured unit

- Good condition (no major rust or structural issues)

- Clean driving records for household members

If your Chevy is stored outdoors long-term, you may not qualify.

Best Coverages for Classic Chevy Owners

Below are the insurance features YOU—specifically as a classic Chevy owner—should look for.

1. Agreed Value (Guaranteed Value) Coverage

The gold standard for classic Chevy insurance. Avoid “stated value”—it’s not the same and may still depreciate.

2. Comprehensive & Collision (Built on Agreed Value)

Protects against:

- Accidents

- Fire

- Theft

- Vandalism

- Storm damage

- Hit-and-run

3. Liability Protection

Even a Sunday cruise in your ’68 Camaro can turn expensive without proper liability coverage.

4. Spare Parts Coverage

Chevy parts aren’t cheap—especially OE or NOS parts. Good policies cover parts stored in your garage:

- SS emblems

- Chrome trim

- Grilles

- Dash clusters

- Restored bumpers

- Body panels

5. Restoration or “Project Car” Coverage

Perfect for:

- Frame-off Chevelle restorations

- C10 builds

- Camaro resto-mods

- Long-term projects

Coverage should increase as you invest more money in the build.

6. Classic Car Roadside Assistance

Preferably with:

- Flatbed towing

- Low-clearance transport

- Battery jump and fuel delivery

- Trip interruption coverage

Classic Chevys deserve better than a standard tow hook.

Classic Chevy Insurance Comparison Table

(Hagerty vs. State Farm vs. American Collectors Insurance)

| Feature / Benefit | Hagerty | State Farm (Classic & Antique Program) | American Collectors Insurance |

|---|---|---|---|

| Coverage Type | Collector Car Insurance | Classic/Antique Vehicle Coverage | Collector Car Insurance |

| Agreed Value Coverage | Yes — true Agreed Value (no depreciation) | Yes, but varies by state & underwriting | Yes — Guaranteed Value |

| Mileage Limits | Flexible plans; options from low-mileage to unlimited hobby use | Limited-use only; generally low annual mileage required | Tiered mileage plans (1,000–7,500 mi/yr) with rollover options |

| Daily Driving Allowed? | No | No (must not be a primary vehicle) | No (hobby use only) |

| Storage Requirements | Garaged or secure indoor storage | Garaged preferred; may vary by state | Garage/secured storage required |

| Eligibility Vehicle Age | Typically 1980 & older, but newer “modern classics” accepted | Varies; often 25+ years, condition-dependent | 1990s–2000s modern classics can qualify |

| Spare Parts Coverage | Optional add-ons; strong for restorers | Limited spare parts coverage (varies) | Included (up to set limit) with optional increased coverage |

| Restoration / Project Car Coverage | Yes — agreed value increases as you restore | Depends on state; not always available | Yes — covers parts + cars in restoration |

| Towing / Roadside Assistance | Hagerty Drivers Club (flatbed towing, discounts, trip interruption) | Roadside assistance available as add-on | Full flatbed towing, roadside support & specialized collector towing |

| Specialty Benefits | Valuation tools, online comps, event coverage, “Cherished Salvage” option | Easy bundle with current auto/home insurance | Inflation-guard coverage, tiered mileage with rollover |

| Driving Record Requirements | Clean record preferred | Standard underwriting applies | Clean record preferred |

| Best For… | Owners of high-value classics, show cars, resto-mods, and rare Chevys | Owners who want to bundle everything with one insurer | Owners who drive occasionally, want best pricing & strong spare-parts coverage |

| Chevy Models Well-Suited | Bel Air, Tri-Five, Chevelle, Camaro, Corvette, Resto-mod Chevys | Drivers of classic Chevys who already use State Farm | C10 trucks, Bel Airs, Camaros, Chevelles, and project cars |

| Typical Price Range | Moderate premiums | Usually low–moderate | Often lowest overall due to collector-only focus |

| Claims Experience | Excellent — collector-focused adjusters | Good, but not classic-specialized | Collector-vehicle specialists handle claims |

| Overall Rating for Classic Chevys | ⭐⭐⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐⭐⭐ |

- Hagerty – Best overall for high-value classic Chevys, show cars, and owners who want specialty benefits + Hagerty valuation tool.

- State Farm – Best for owners who already have State Farm and want everything bundled for simplicity.

- American Collectors – Best for budget-friendly premiums, C10 trucks, project Chevys, and owners who want mileage rollovers + strong spare parts coverage.

How Much Does Classic Chevy Insurance Cost?

The good news? Chevy collector car insurance is usually cheaper than standard auto insurance, because:

- Cars are driven less

- Better storage

- Lower accident rates

- More responsible owner demographics

Pricing factors include:

- Your Chevy’s agreed value

- Model (Bel Air vs Camaro vs C10)

- Zip code & theft/storm risk

- Mileage tier

- Driver history

Expect a wide range: $150–$600/year for most drivers and popular models.

How to Get the Best Classic Chevy Insurance Policy

Use this step-by-step plan to secure coverage that protects your car’s full value.

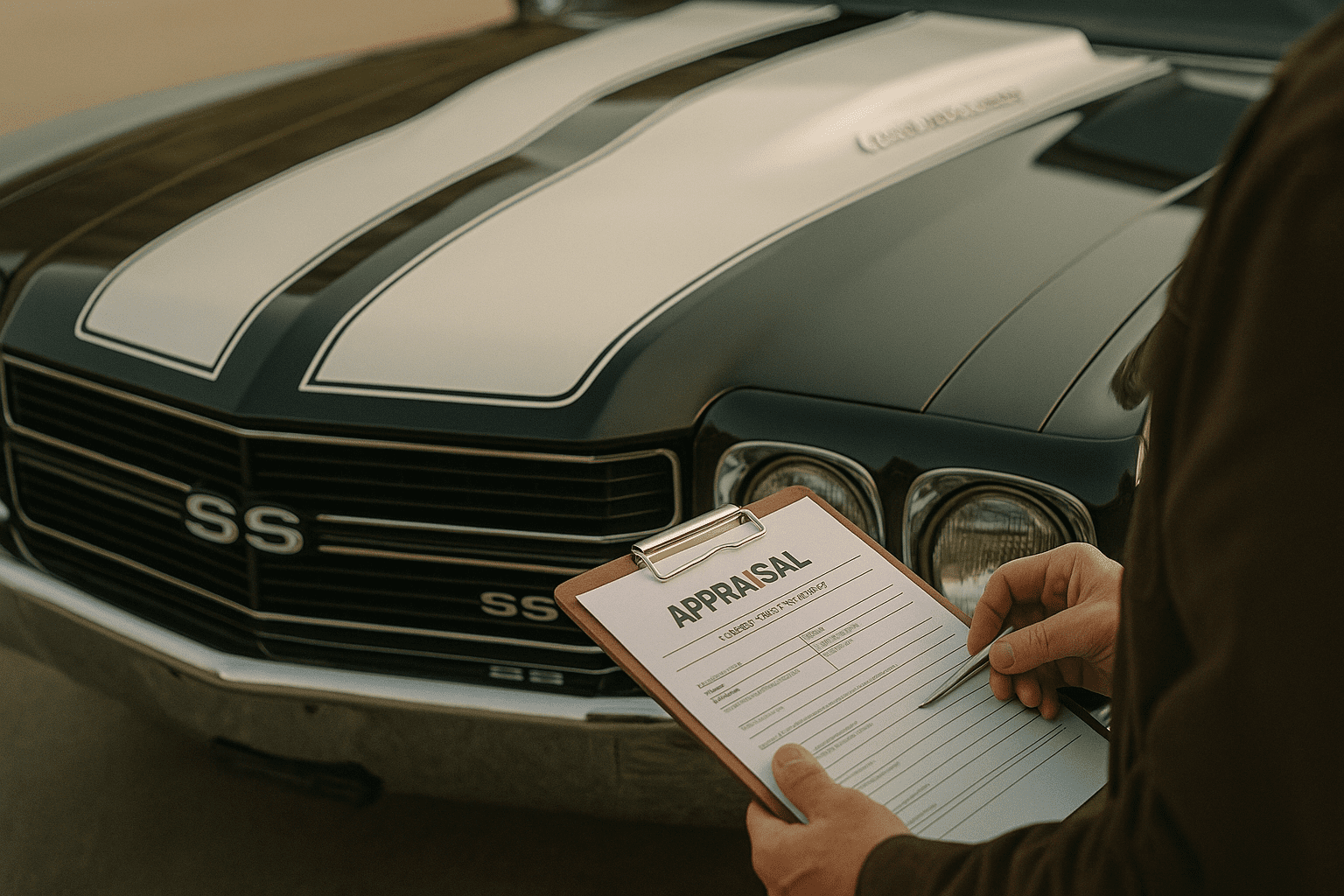

Step 1: Document Your Classic Chevy

Collect:

- High-quality photos (interior, exterior, engine, frame)

- Receipts for parts, upgrades, and restoration work

- Appraisals or value estimator results

You can also cross-check pricing and condition-based values using NADA’s classic car value guide, which many insurers reference during underwriting.

Step 2: Determine Actual Usage

Be honest about mileage:

1,000 miles? 3,000? 5,000?

Your premium depends on it.

Step 3: Evaluate Storage

Insurers prefer locked garages or buildings. Upgrade storage if needed.

Step 4: Get Quotes from Collector Specialists

Compare:

- Agreed value

- Spare parts limits

- Mileage tiers

- Roadside assistance

- Restoration coverage

- Restrictions

Step 5: Review Your Policy Annually

Classic Chevrolet values rise—your coverage should too.

Classic Chevy Insurance for Specific Models

Tri-Five Chevy Insurance (1955–1957 Bel Air, 210, 150)

High-demand classics with rising values → must use agreed value.

First-Gen Camaro Insurance (1967–1969)

Muscle car premiums are higher but stable; limited-use discounts help.

Chevelle SS Insurance (1964–1972)

Insurance should reflect originality, big-block options, and restoration condition.

Classic Chevy Truck Insurance (C10 & C/K Series)

C10 values have surged → important to update agreed value yearly.

Common Mistakes Chevy Owners Make With Insurance

Avoid these expensive errors:

❌ Insuring a classic Chevy with a standard auto policy

You WILL lose money if the car is totaled.

❌ Not disclosing modifications

Insurers can deny claims if you hide mods.

❌ Underinsuring a restored vehicle

If you put $40k into your Tri-Five restoration but insure it for $25k…

that’s all you’ll get in a payout.

❌ Assuming project cars don’t need insurance

Garage fires and thefts happen — protect the investment.

Real Examples from My Classic Chevy Policies

Example 1 — 1957 Bel Air (Agreed Value: $42,000)

- Premium: ~$380/year

- Storage: locked garage

- Annual miles: 1,500

- Underwriter wanted: 12 photos, VIN, receipts

- Claim experience: smooth, full payout after minor rear-end repair

Example 2 — 1972 C10 (Driver-Condition)

- Agreed value: $18,000

- Premium: ~$290/year

- Allowed 5,000 miles/year

- Insurer asked for underbody pics (rust check)

Example 3 — 1966 Chevelle Project

- Non-running, partially torn apart

- Storage-only policy

- Premium: ~$120/year

- Coverage included fire, theft, and damage to stored parts

How Insurance Fits Into Your Chevy Ownership Strategy

Insurance is just one pillar of protecting your classic Chevy. Connect with:

- Classic Chevy Buyer’s Guide

- Classic Chevy Parts Guide

- VIN Decoder Tool

- Classic Chevy Value Estimator

- Restoration Cost Guides

- Guide to Buying Classic Chevrolets

FAQs About Classic Chevy Insurance

Is classic Chevy insurance cheaper than regular insurance?

Yes—because mileage is lower and cars are stored more securely.

What qualifies a Chevy for collector car insurance?

Age (25–30+ years), limited use, garage storage, and good condition.

Do I need agreed value coverage for my classic Chevy?

Absolutely. It’s the only way to protect the real market value of your Chevy.

Can I daily-drive my classic Chevy with collector car insurance?

No. Policies restrict daily commuting.

Does collector insurance cover spare parts?

Yes—most policies include dedicated spare parts protection.

Can I insure a project car that’s being restored?

Yes—as long as it’s stored properly. Coverage can increase as the build progresses.

Safety, Transparency & Compliance Disclaimer

This guide is general informational content, not legal or financial advice.

Always review policy documents carefully and verify coverage with your insurer.

Insurance requirements vary by state, provider, and personal driving record.

Last updated: 12/6/25 — This guide is reviewed annually for accuracy, policy changes, and new insurance trends affecting classic Chevy owners.

About the Author

Gary Thompson — Founder of OldChevys.com

Gary is a lifelong Chevy enthusiast who has owned, restored, and insured multiple classics, including Tri-Fives, Novas, Chevelles, and C10 trucks. With over 20 years of experience attending shows, swap meets, and auctions, he helps classic-car owners avoid costly mistakes through detailed, experience-backed guides.